A look at the latest preliminary BLS Current Employment data shows that the United States Non-Farm Employment may have increased by a seasonally-adjusted 4.8 million positions in June 2020. If these numbers hold up, the gains would translate into an economy that has “recovered” 36% of the jobs displaced since March 2020.

While the data for June only captures data from the middle of the prior month to the middle of the given month (as is the BLS standard practice) a deep analysis of these preliminary numbers reveals that out of all low-level industries (with preliminary numbers available for June) only 4 out of 132 industries recouped all the jobs they lost this last April and May. This is even less impressive than it sounds when you look at the industries that recovered and see how little they were originally impacted:

Over 93% of BLS-tracked industries in June have seasonally adjusted employment levels nationwide below what they were in March. It’s currently unclear to me (and probably everyone else) what percentage of job losses are due to the COVID-19 shutdowns, and what continuing job losses are due to related decreases in consumer spreading, or are caused by unrelated industry shifts.

Still, with the limited information we have, below are four big takeaways for June 2020. (As always, the data is from the raw United Stated Bureau of Labor Statistics Current Employment Data, processed using Python, and graphed with R using the techniques and methods described in this post.)

Takeaway 1: The Show Is Not Going On

The Motion Picture and Sound Recording Industry continued its industry-wide employment crisis last month and this is now the industry worst-hit by COVID-19, as a percentage of jobs lost (among industries in which preliminary June data was available). Only “Performing Arts and Spectator Sports” was in the same ballpark, still down 45% in employment from March.

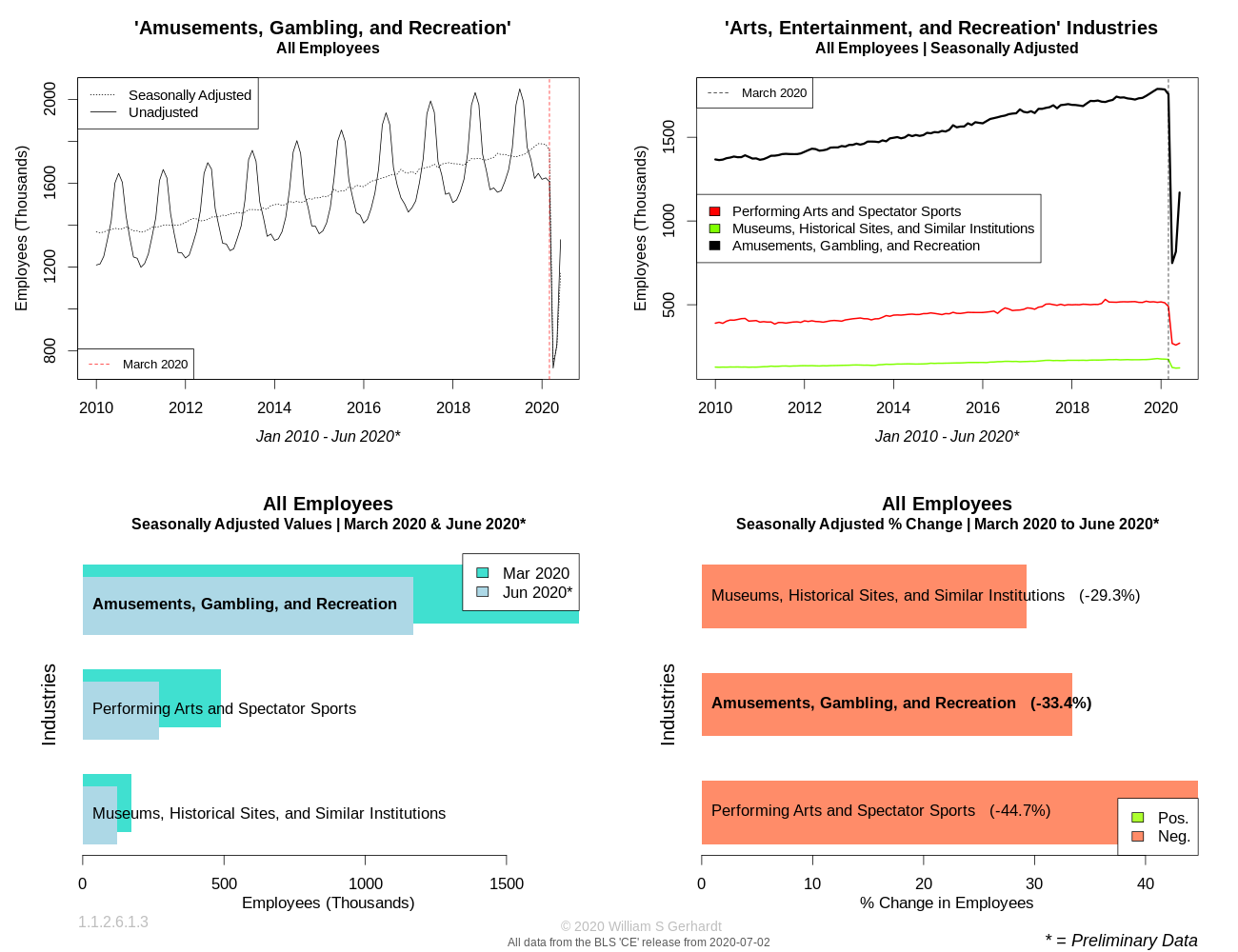

While the lowest granular level of U.S. industry employment is on a two-month delay, next month we can expect to see that the lion’s share of the job losses in this category were due to the near implosion of the “Motion Picture and Video Exhibition” industry, which lost a whopping 85% of employees in the months of April and May 2020. (Only the BLS category of Racetracks was close among low-level industries, with racetrack employment dropping 84% in the same period.)

Takeaway 2: Fitness and Recreation Get a New Twist

For those tired of receiving their entertainment from re-watching old episodes of ‘Friends’, following the daily stock market, weight training in their living rooms, or reading books (!), the broadly defined “Amusement, Gambling and Recreation industries”—which encompasses everything from bowling centers, to marinas, to casinos—continued to build on its May 2020 rebound:

The re-opening of this industry is giving leisure and exercise-seekers an opportunities to enjoy themselves or improve their bodies; while at the same providing a potentially once-in-a-lifetime experience of doing these things during a raging and uncontrolled epidemic.

Takeaway 3: Dental Offices Are ‘Filling’ Jobs Again

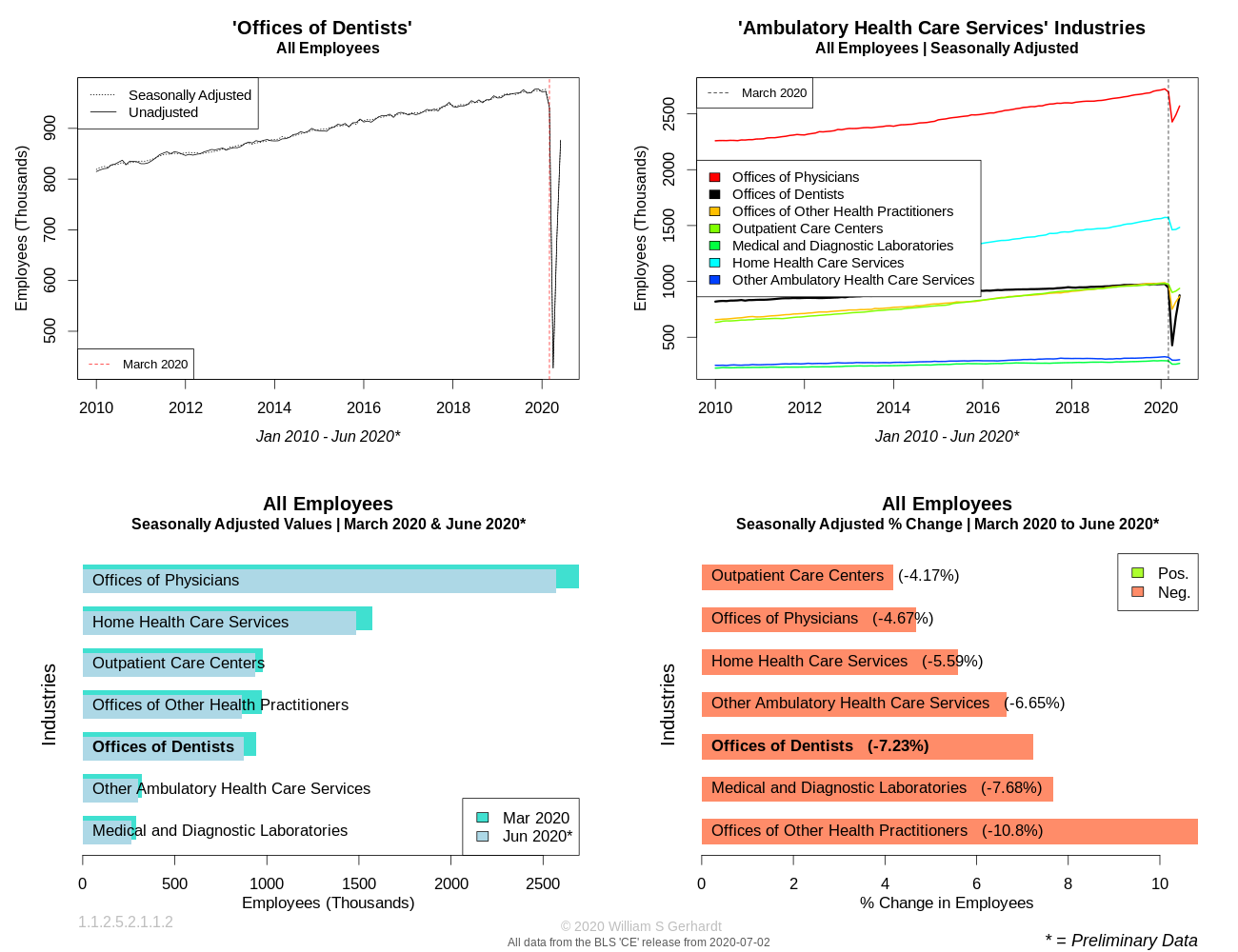

I have limited wisdom to share on this well-rooted industry, but for now you can get those teeth nice and polished for the next video conference call:

The June 2020 numbers represent a major restoration in employment from prior months, as Dental Offices were among the industries most impacted by the first wave of COVID-19 shutdowns.

Takeaway 4: Monetary Authority Employment is Becoming Marginally Less Boring

Finally, updated BLS numbers for April and May showed showed slight signs of life in Central Bank employment, and this small sector is now posting 1% job gains across April and May. Preliminary June 2020 numbers were flat, but if they behave like the April and May numbers they are likely to be revised upward in coming months:

In recent months the U.S. Federal Reserve added a trillion dollars to their balance sheet and publicly claimed to purchase large amounts of corporate bonds and even ETFs. A substantial hiring effort would logically seem to be necessary to handle vetting and oversight of these increased purchases, and I can only hope that the 1% increase in Central Bank employment in April and May (revised upward from previous estimates) helped them with that.

While I am still waiting to see (as we probably all are) what the labor market in late June and early July will turn out like, some future posts on this blog will look at what happened to hours and aggregate employee earnings during the Spring COVID-19 shutdown.

(Also, a footnote: An official-looking email for this blog is now up and running. You may now email me, if you like, at a new site email address: contact@creativedataideas.com.)